Scaling for Business

This week, I would like to explore another subtopic related to scaling: scaling in business. Today’s post will be an introduction to the topic. I may come back and explore business scaling some more later, as there is much to say about it.

This work is part of the Scaling in Human Societies project, which is funded by Open Philanthopy’s Living Literature Review grant. A write-up on the Scaling site is also in progress. As always, the work here is my own and does not represent the views of Open Philanthropy.

Scaling Defined

It occurred to me that, even though I have been working on this Scaling project for about a year, I have never attempted to define the term. Part of the issue is that “scale” is a common enough word that I have taken it for granted. But let us attempt to be rigorous.

For this project, I have taken “scale” to refer to how a system changes with size. Of the systems we may consider, the biggest focus has been on cities. Over several posts, such as this one, we have seen that various socioeconomic quantities related to cities, such as total economic output, do not generally vary linearly in city size. We have also considered several aspects of sustainability as they relate to civilization size. There are many interesting scaling observations about nonhuman systems as well, such as the the Hertzsprung-Russell diagram relating star brightness and temperature, and some examples discussed in Geoffrey West’s (2017) Scale, but those are outside of the scope of the project.

Discussion about the growth dynamics of companies goes back a long way, with Edith Penrose’s (1959) The Theory of the Growth of the Firm being a classic in the field. Nevertheless, the theory of scaling in companies is not as well develop as the theory of scaling in cities. Even the question of what “scale” means is not fully settled.

Bohan et al. (2024) define business scaling as a “time-limited process of exponential growth”. They are thus focusing on the growth process itself, rather than how two business of different, static sizes differ from each other. The metric by which business size is measured may be the number of employees or total revenue.

The “exponential” in the definition of Bohan et al. (2024) distinguishes scaling from growth, which is more general and may or may not be exponential. An exponential process is characterized by the growth rate being proportional to the current size. In an idealized form, a bank account that gains interest of 2% per year, a population size that grows at 1% per year, or a business that grows at 20% per year are exponential processes. The basic form of an exponential function looks like this.

Here, y is the quantity of interest, such as business size; t is time; b is the growth rate; a is a constant; and e is Euler’s number, which is approximately 2.71828. The doubling time, or the time it takes for y to double, is about 1.44/b. The word “exponential” is frequently misused in the press to mean simply “fast” or “a lot”, and here it is important that we use it correctly.

Finally, the “time-limited” aspect of the definition of Bohan et al. (2024) is needed, since exponential growth is a finite system must necessarily end at some point. A company that is scaling will eventually saturate its potential customer base, if it does not reach some other limit to growth earlier. Scaling is thus a process that begins and ends.

Bohan et al. (2024) add two elaborations which, though not strictly necessary in their definition, clarify the process of scaling. The first is that there should be increasing returns to scale. A business can be viewed as a structure that transforms inputs (capital, labor, etc.) that can be monetized into revenue. A viable business must have revenue exceeding inputs. Increasing returns to scale means that the ratio between revenue and input should increase with business size, giving large businesses a competitive advantage over small businesses. This, according to Bohan et al. (2024), is the key factor that drives scaling. The second elaboration is that the internal structure of a business should change with scale. We will come back to that point later.

Palmié et al. (2023) define scaling as

an increase in the size of a focal subject that is accompanied by a larger-than-proportional increase in the performance resulting from the said subject.

In contrast to Bohan et al. (2024), the rate of growth is not inherent to the definition, but increasing returns to scale are. Palmié et al. (2023) allow “size” to be defined over four metrics and thus give rise to four kinds of scaling: market scaling, volume scaling, financial scaling, and organizational scaling.

Shepherd and Patzelt (2020) define scaling as “spreading excellence within an organization as it grows”. This definition highlights the challenges that growing companies face: the replacement of venture founders by professional managers and the accumulation of bureaucracy. Here, “excellence” refers to those practices that are necessary to organizational thriving.

Drivers of Scaling

Businesses in the world range in size from sole proprietorships to Walmart, the largest corporation in the world by headcount at 2.1 million employees. The range of sizes is governed by a balance between the advantages and disadvantages of scale, which are influenced by a firm’s specific industry, jurisdictional factors, factors related to the specific firm, and other considerations. If there were no advantages to scale, we would expect all economic activity to be conducted by sole proprietors. If there were no disadvantages, we would expect all economic activity to be conducted by a single megacorporation. Therefore, to understand how we end up with the set of business sizes that we see, we need to understand both the drivers and barriers to scaling.

Bohan et al. (2024) identifies three factors that motivate scaling. The first is economies of scale. This idea, which goes back to Adam Smith’s (1776) The Wealth of Nations, is that goods can be produced at a lower per-unit cost by one larger firm rather than two smaller firms. Formally,

where TC is the total cost function, X is some good, and Q_1 and Q_2 are production quantities. If the opposite holds, then the phenomenon is called a diseconomy of scale.

Economies of scale can manifest in physical terms. For example, Ros Chaos et al. (2020) examine the cruise ship industry and find that per-passenger costs of delivering cruises decreases with increasing size of the ships, up to a size of 120,000 tons, beyond which the per-passenger costs increases. At present, the largest cruise ships in the world are the Icon of the Seas and Stars of the Seas, which entered service last year and this year respectively, and each have a gross tonnage of 248,663 tons and a capacity of up to 7600 passengers, showing how the market is not monolithic and that there is not a sharp “ideal size” to which all cruise ships converge.

Wind turbines tend to be cheaper per kilowatt-hour of electricity produced when they are larger, up to practical limits of engineering and materials, which is why wind turbines tend to become larger over time. By contrast, buildings tend to be more expensive per square foot for taller buildings, a diseconomy of scale for skyscraper size, a phenomenon that is partly the result of elevator costs. Skyscrapers exist not because of economies of scale, but to take advantage of the scarcity of commercially valuable real estate.

The second of Bohan et al.’s (2024) drivers of business scaling is economies of scope. These are closely related to, and are often confused with, economies of scale. Economies of scope are situations in which it is cheaper, on a per unit basis, to offer multiple products than for separate firms to offer the products individually. “Synergy” is the corporate jargon for this effect and is a major motivator behind corporate mergers, though as a McKinsey report documents, synergies often don’t result from mergers as hoped.

Economies of scope can emerge from scale-free resources, which in an idealized sense are resources that have the same cost regardless of how much production they are applied to. For example, a patent has a certain cost of develop, but once developed, can be applied to many different products at low marginal cost. Few resources are truly scale-free. For example, Arifoglu and Tang (2019) document how luxury brands can dilute and lose value through over-licensing, as happened to Gucci, negating the idea that even a brand name is a true scale-free resource.

The third of Bohan et al.’s (2024) drivers of business scaling are demand-side economies, such as network externalities. Network externalities are the phenomenon of a product being more valuable when more people use it. A potent example is Metcalfe’s Law (see Metcalfe 2013), which holds that the value of a telecommunications network is proportional to the square of the number of people using it. The intuition behind the law is that the value of the network is proportional the number of possible dyadic connections, and for a network with n nodes, there are n(n-1)/2, or O(n^2), possible connections. This is why networking standards such as Ethernet (invented by the same Robert Metcalfe as Metcalfe’s Law) and TCP/IP, social networks such as Facebook, and messenger apps such as WhatsApp become so dominant.

Underpinning all three mechanism are learning economies. I wrote about learning curves on this blog last year and a longer paper later in the year, where I argued that learning effects, though real, are often overestimated in the literature and in policy. The external value of learning is of most interest to policy makers, but the internal value of learning—that which is captured by the firm engaged in production—is of interest to the company and a motivator for large size.

Barriers to Scaling

Obviously there are barriers to business scaling, as not all of the world’s business activity occurs under a single megacorporation. There are many barriers, but I will focus on the coordination problem.

As Bohan et al. (2024) explain, for a company with n employees, there are n(n-1)/2 possible dyadic connections between the employees. Put another way, if there are n employees, each employee can communicate with n-1 other employees. For a small company with n<10 employees, this hardly matters. For a large corporation with tens of thousands of employees, it is clearly impossible to coordinate such a large number of people without several layers of middle management, as the CEO could quickly become overwhelmed with communication in a flat hierarchy.

McAfee and McMillan (1995) find that the cost of operating a hierarchy grows with the hierarchical distance, or the number of layers of management from the lowest level employee to the CEO. This quantity grows at a slow rate—logarithmically in the number of employees—but enough to to put a noticeable difference between large and small firms. A company with 10,000 employees should have, roughly, twice the hierarchical distance as a company with 100 employees.

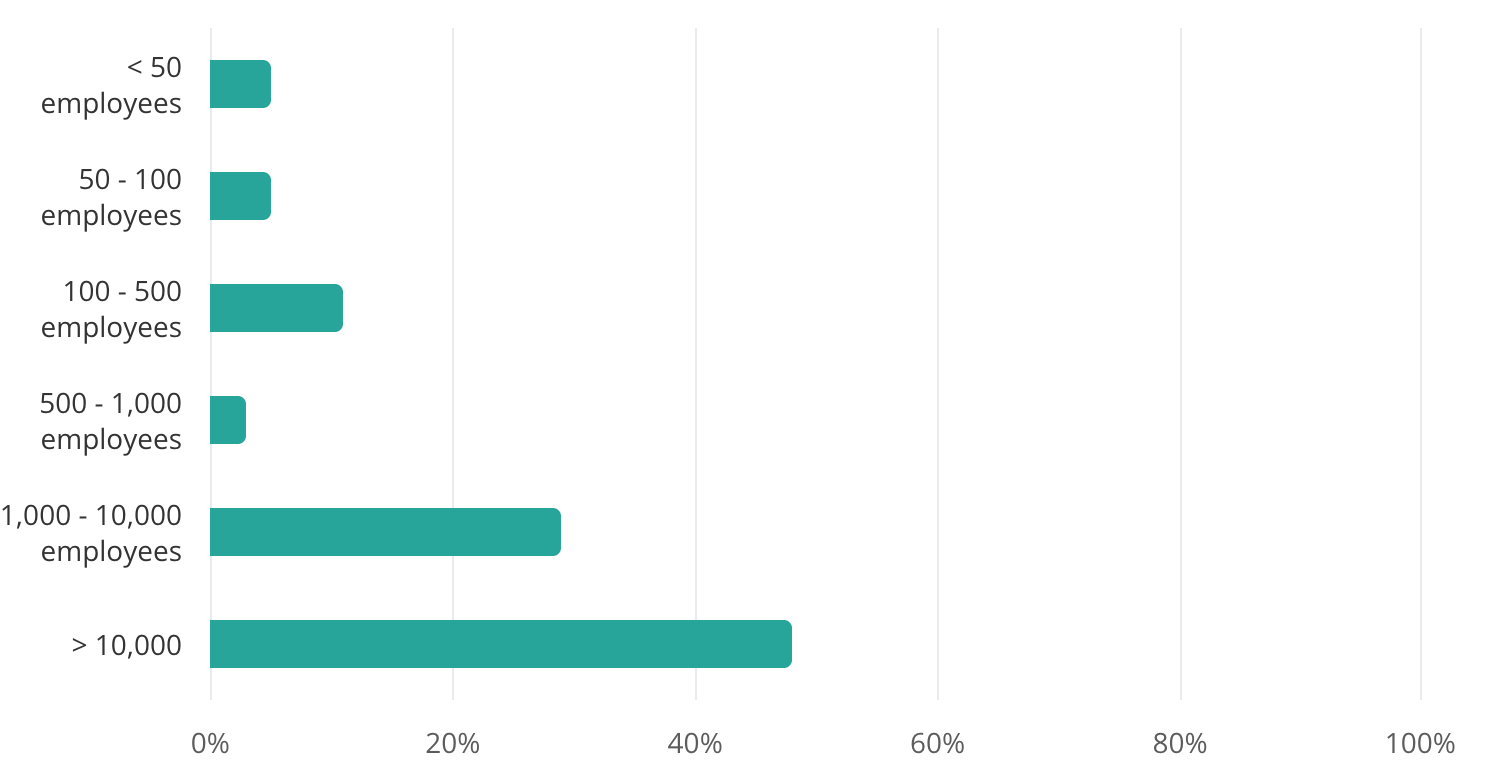

The above chart shows that the proportion of the employees that are managers grows with the size of the company, though I’m sure what is happening in the 500-1000 employee companies. For large (>10,000 employees), that portion is nearly half, and so the cost of maintaining the necessary hierarchy is indeed formidable. This sounds analogous to what I found in my elevator post, which is that, by necessity, the proportion of a building that is devoted to elevator space grows in the size of the building, placing a practical limit on the height of buildings. Perhaps there is an analogous practical limit on the size of functional companies, lest their resources are completely consumed by management. There is another analogous problem with road space in large cities which I hope to address in a future post.

Conclusion

Like cities, companies exist in sizes ranging from a single person to millions of employees. Like cities, companies exist in an equilibrium between economies of scale and diseconomies of scale, which is why we are not all sole proprietors, nor do we all work for a single global megacorporation. What that equilibrium size is depends on the industry, on the regulatory environment, on the company culture, and on a huge number of other factors.

There is quite a bit more to say. Why do firms tend to be bigger in some industries than in others? Do we expect new communication technology to lead to bigger firms, smaller firms, or to have no effect? I certainly hope to come back to this topic.

Quick Hits

A few weeks ago saw the Trump administration’s 20 point proposal for peace in Gaza. Following two years of horror, starting with Hamas’ barbaric attacks of October 7, 2023 and severe, seemingly indiscriminate bombing on Gaza, the ceasefire has been widely welcomed. I find it remarkable that there has been a positive reception from most quarters, including people and entities who are generally more sympathetic to Israel, from those generally more sympathetic to the Palestinians, and from people who rarely otherwise have much positive to say of what comes from the Trump administration. The Council on Foreign Relations has a useful summary.

There are still formidable obstacles between today and a lasting peace in Gaza, not the least of which is the role of Hamas. I wrote two years ago, and stand by the conclusion today, that any political power for Hamas is incompatible with peace in the region. Matthew Levitt at Foreign Affairs assesses the difficulty in disarming Hamas. Conversely, Israeli Prime Minister Benjamin Netanyahu will have difficulty appeasing hardliners in the cabinet who oppose peace.

I just barely missed it for the last post, but Reuters assesses the effectiveness of the recent federal crime surge in Washington DC. The conclusion is about what I would have expected: some classes of crime went down, some were unaffected or went up, and it was all more or less within the normal range of fluctuation. It therefore cannot be concluded that the surge had a significant impact on crime levels. For critics of the policy, the issue is not whether the surge was effective but suspicion about whether crime reduction was the real purpose. Such an overt federal role in local law enforcement would also be radical departure from traditional ideas of federalism.

If your first instinct to projections of huge electricity demands from data centers in the coming years is skepticism, you might enjoy this 1999 article from Forbes entitled “Dig More Coals -- the PCs are Coming”. It too painted an alarmist picture of spiking energy demand, and consequent environmental hazards, resulting from what was then the new consumer technology of the Internet. But the impact is real; researchers at Lawerence Berkeley Livermore Laboratory found that data center electricity usage in the US grew from 1.9% to 4.4% of total electricity from 2018 to 2023.

Richard Morrison has written “The Managerial Tyranny of Boomer Environmentalism”, in response to a piece by Steven Hayward. Morrison’s essay is overly polemic in my view, but he raises some important points of soul searching for the movement.